What is it about first quarters? Looking back at the past decade, the Morningstar US Market Index declined in the first quarters of 2025, 2022, 2020, and 2018. This time last year, I recapped a “doozy” of a quarter in which the US stock market entered correction territory. DeepSeek AI, tariffs, and stagflation fears all contributed to a “risk-off” vibe in early 2025.

Well, I’d say the first quarter of 2026 has been another doozy. A “Software Selloff” (or “SaaSPocolypse”), panic in private credit, war in the Middle East, and, yes, more tariff turmoil have all roiled markets. Treasury yields have risen on inflation fears. The overall numbers for the broad stock and bond markets may not be pretty, but they aren’t disastrous.

Morningstar’s index range reveals pockets of both strength and weakness. Here are two losers and three winners from early 2026.

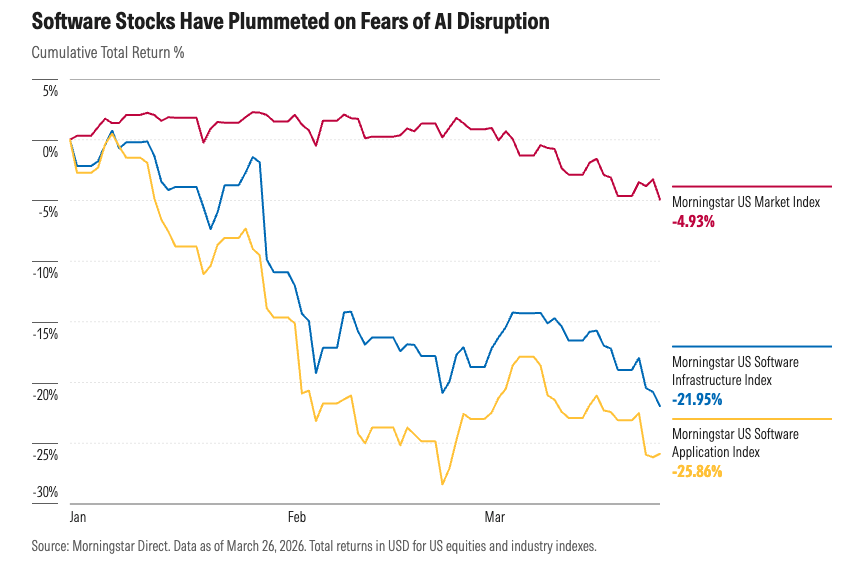

Q1 Loser Number One: Software Stocks

Warren Buffett famously shied away from technology. Not only did email and smartphones long fall outside his personal “circle of competence,” but he also mostly viewed the sector as too fast-moving and difficult to forecast for investing.

“Fast-moving” and “difficult to forecast” seem apt descriptions of the technology sector today. Artificial intelligence has been the dominant market theme for the past three years, propelling beneficiaries like Nvidia NVDA to once-unthinkable valuations. But the first quarter of 2026 has been all about the disruptive potential of AI. Doomsday scenarios about business models threatened and jobs rendered obsolete sent swaths of stocks down sharply.

The Software Infrastructure and Software Application industries have been especially hard-hit. Microsoft MSFT and Oracle ORCL are stalwarts of the former grouping, while Salesforce CRM and ServiceNow NOW belong to the latter. All have been pummeled.

Is the selloff justified, or has it created buying opportunities? According to Morningstar Equity Research, AI is not a universal disruptor of all competitive advantages, and in some cases, share price pullbacks are overdone. Eric Compton, director of research for technology, summarized the team’s views in this interview.

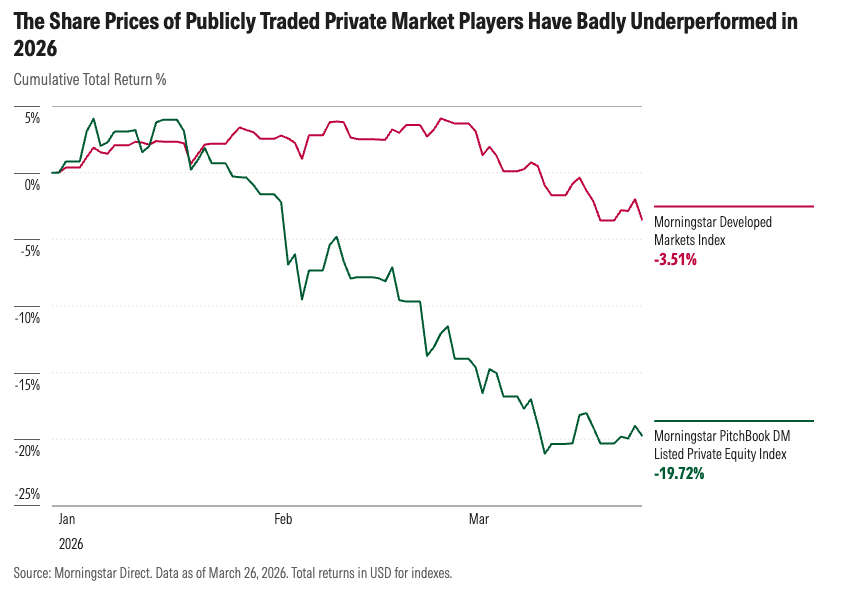

Q1 Loser Number Two: Private Markets Investors

Private debt markets are showing signs of stress. According to Morningstar DBRS credit research, defaults among distressed middle-market borrowers have risen over the past year. The AI panic has only compounded problems. Lacking transparency into private funds’ software holdings and their prices, some investors have rushed for the exits—to the extent they can.

Unlike traditional private funds, broadly accessible semiliquid funds allow intermittent withdrawals. Vehicles run by Blue Owl, Blackstone, and others have been overwhelmed by redemption requests. The experience has provided a cautionary tale for strategies that sit at the intersection of public and private markets.

The share prices of publicly traded private market investors act as a barometer of this trend. The Morningstar PitchBook Developed Markets Listed Private Equity Index, which includes companies like Blackstone BX, KKR KKR, and Partners Group PGHN, has outperformed its broad equity market equivalent in recent years, tracking the boom in private market investing. This year, the index is down sharply. Its losses have dragged down the entire financial-services sector.

Will the growth of private markets slow? You’ve heard us talk about the rise of private equity and private debt as one of the key investment trends of recent years. A shift in capital formation has seen some $16 trillion in private capital fund startups, buy out companies, and lend directly. Much of that money is locked up. But more trouble could be ahead, especially on the debt side. Morningstar DBRS says private credit downgrades have outnumbered upgrades by more than three to one in early 2026. Its outlook for the rest of 2026 is negative.

Time to shift gears. It wasn’t all gloom and doom for investors in the first quarter. Let’s talk about some investments that soared.

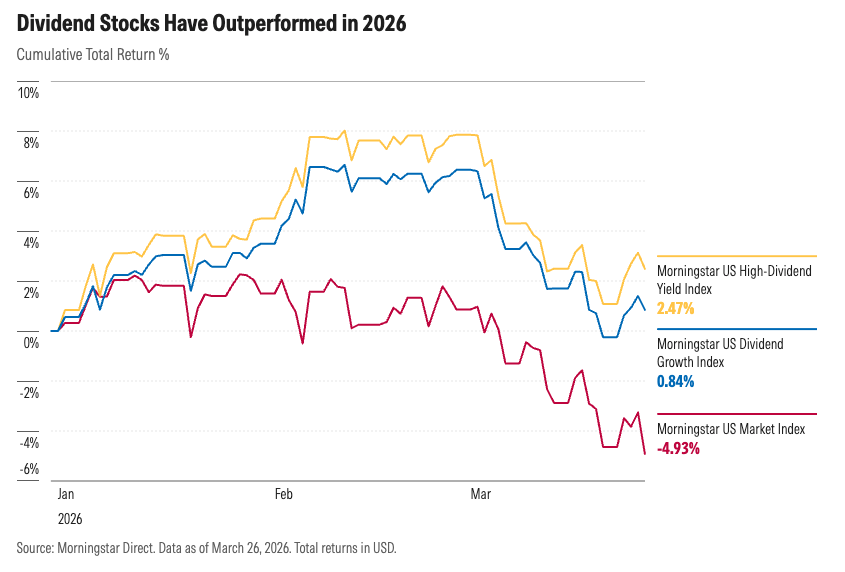

Q1 Winner Number One: Dividend Stocks

I wrote recently about HALO, a fun new Wall Street acronym standing for Heavy Assets, Low Obsolescence—that is, the kind of company that can’t be disrupted by AI. The flip side of the aforementioned software selloff is the popularity of businesses owning physical infrastructure. You can’t replace an electricity grid with an AI bot. Oil still fuels the global economy (pun intended).

HALO has lifted the dividend-paying section of the stock market. Both the Morningstar US High Dividend Yield Index and the Morningstar US Dividend Growth Index are ahead of the broad market this year. Both lagged during the AI boom of 2023-25 and in several prior years of tech enthusiasm.

Before getting too excited, equity-income investors should remember that we’ve seen several recent periods of dividend stock leadership fade. Dividend-paying stocks also outperformed briefly in early 2025. Whatever the near future holds, dividend-payers hold merit as sources of income and a lower-volatility means of long-term equity market participation.

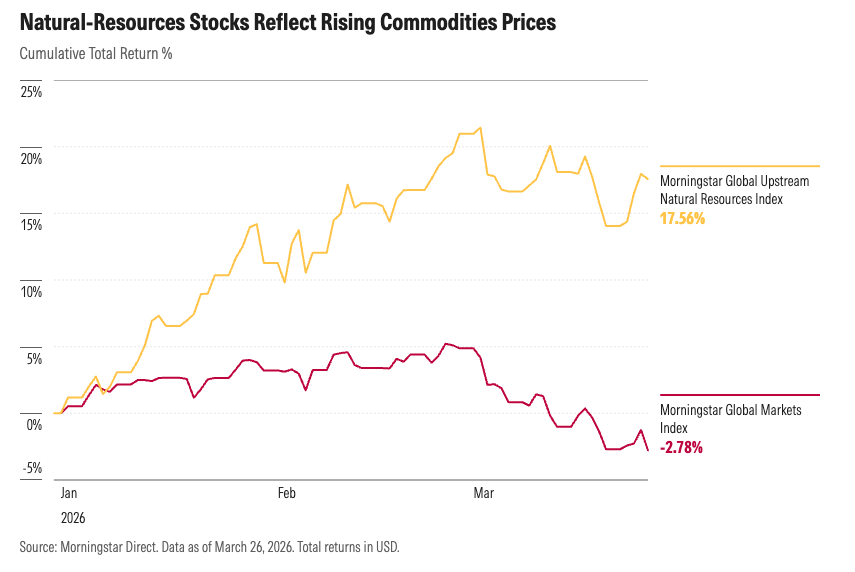

Q1 Winner Number Two: Commodities

The Iran war has caused an energy price spike. The Morningstar Global Upstream Natural Resources Index, which tracks the shares of companies whose earnings are highly leveraged to commodity prices, reflects not just higher oil prices but also a broader boom. Shares of agriculture-related businesses like Corteva CTVA and Nutrien NTR have also soared.

It’s reminiscent of 2022, when commodities also diversified stocks and bonds. Four years ago, generationally high inflation and a harsh monetary policy response wreaked havoc on both major asset classes. That year, as in this, geopolitics sent oil prices surging. For investors who can stomach their volatility, commodities can contribute to a diversified portfolio.

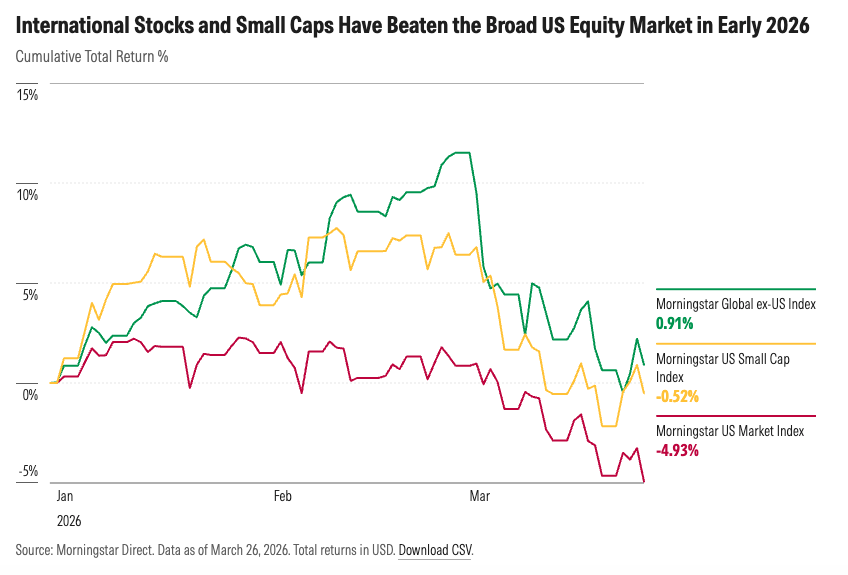

Q1 Winner Number Three: Equity Diversification

I’ve mentioned that commodities have been a good diversifier this year. Bonds less so. I’ve also mentioned that there has been a rotation from high-tech growth stocks to the dividend-rich HALO trade, which clusters on the value side of the market.

What I haven’t yet covered is the fact that international stocks and US small caps have beaten the broad US equity market so far in 2026. Neither asset class has shot out the lights. But the first quarter has rewarded equity portfolios diversified by market capitalization and geography, even though the US dollar has strengthened. Being light on technology stocks has actually been an advantage for both asset classes in 2026.

As a reminder, the past 15 years have been characterized by US large-cap-growth stock leadership. As a result, many US investors have neglected global exposure, small caps, and value. Historically, those asset classes have experienced cycles of outperformance—the first decade of the 2000s providing one example. International stocks also posted a strong year in 2025. Only time will tell if we’ve moved into a lasting period in which equity diversification pays off.

As for the Rest of 2026 …

If 2025 is anything to go by, 2026 could get worse before it gets better for US stocks. Who can forget the plunge following the tariff announcements in early April of last year? The broad US stock market declined by more than 10% in just two days.

But the first quarter of 2025 did not portend a down year. Quite the contrary. The Morningstar US Market Index rebounded powerfully in mid-2025 and finished the year up roughly 17%, thanks to AI enthusiasm (and perhaps the TACO Trade). Investors who rode out the volatility in early 2025 were rewarded by year-end.

What about other rough first quarters? Well, early 2020 brought a “Pandemic Panic,” followed by a strong recovery later in the year. Both 2018 and 2022 were down years overall, with the pain starting in the first quarter.

Have a prediction for how the rest of 2026 unfolds? Email me at dan.lefkovitz@morningstar.com. It doesn’t have to be a number; direction is fine, as are asset-class winners and losers. I’ll keep track of your calls.

Also published on Morningstar.com.

©2026 Morningstar. All Rights Reserved. The information, data, analyses and opinions contained herein (1) include the proprietary information of Morningstar, (2) may not be copied or redistributed, (3) do not constitute investment advice offered by Morningstar, (4) are provided solely for informational purposes and therefore are not an offer to buy or sell a security, and (5) are not warranted to be correct, complete or accurate. Morningstar has not given its consent to be deemed an "expert" under the federal Securities Act of 1933. Except as otherwise required by law, Morningstar is not responsible for any trading decisions, damages or other losses resulting from, or related to, this information, data, analyses or opinions or their use. References to specific securities or other investment options should not be considered an offer (as defined by the Securities and Exchange Act) to purchase or sell that specific investment. Past performance does not guarantee future results. Before making any investment decision, consider if the investment is suitable for you by referencing your own financial position, investment objectives, and risk profile. Always consult with your financial advisor before investing.

Indexes are unmanaged and not available for direct investment.

Morningstar indexes are created and maintained by Morningstar, Inc. Morningstar® is a registered trademark of Morningstar, Inc.