“How has the stock market gone up in the face of all this?” It’s a question I’ve fielded repeatedly from investors unnerved by tariffs, the US government shutdown, debt and deficits, and other macroeconomic worries. Clearly, enthusiasm for artificial intelligence, the most promising technology since the internet (or the steam engine, depending on who you ask), is overshadowing all the risks out there.

Where the worrywarts seem to have prevailed is in currency markets. The first six months of 2025 were the worst for the US dollar in more than 50 years. While it has rebounded since, the dollar’s value is still down for the year against developed-markets currencies like the euro and yen, as well as many emerging-markets ones, like the Mexican peso. My colleague Valerio Baselli attributed the decline to “mounting doubts about US fiscal strength and capricious trade policy.”

Why Does a Weakening US Dollar Value Matter to Investors?

If you’re not a currency trader or planning a Tuscan holiday, does a weaker dollar matter? Well, it certainly has investment implications, both positive and negative. Here, I’ll focus on three asset classes that have been profiting from a weakened dollar in 2025, then contemplate the future for those areas and the currency.

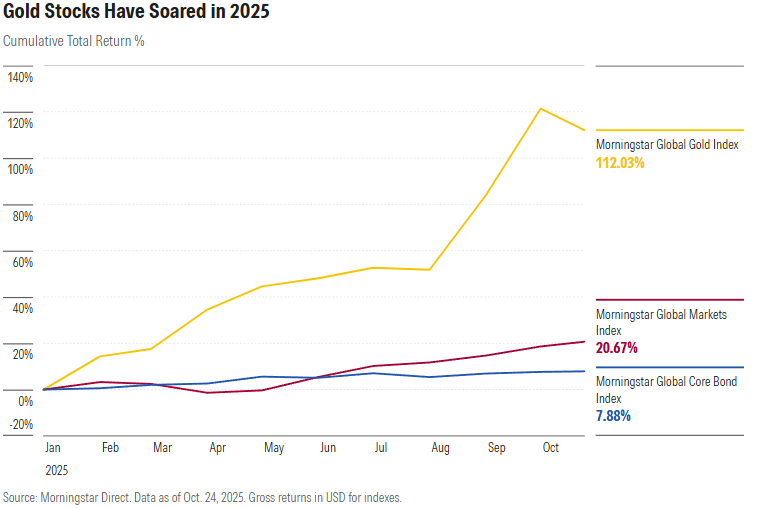

Outperformer #1: Gold Stocks

As newlyweds, Costco shoppers, and "gold bugs" know, the price of the “yellow metal” has soared in 2025. Check out the returns for the Morningstar Global Gold Index, which includes the shares of gold miners, relative to the broad stock and bond markets through the first three quarters of 2025. With the gold price having surpassed $4,000 per ounce in early October (before retreating a bit), mining companies like Newmont NEM are booking massive profits.

What’s the connection between gold and the dollar? In explaining the gold price’s recent runup, Jon Mills of Morningstar Equity Research writes: “Safe-haven buying is a major driver.” In that sense, gold competes with the dollar, which has often appreciated during “flights to safety,” including the 2008 financial crisis and the covid pandemic.

“Many central banks around the world have been on a quest to ‘de-dollarize’ their reserve assets,” writes Morningstar’s Amy Arnott. Evolving trade policy, deficits, lower interest rates, and politics have all raised questions about the US and its currency. Washington’s sanctions against Russia in the wake of the Ukraine invasion were seen by some as a “weaponization of the dollar.” So, moving into gold is partly about diversification in an uncertain world.

Skeptics dismiss gold’s limited utility. Unlike stocks, bonds, and property, it produces no cash flows. Yes, there’s jewelry and some industrial applications, but speculation is the main price driver. As Arnott has shown, the gold price has gone through long periods of weakness—such as 1987 through 1999. “[I]t’s probably not the ideal time to buy gold when it’s already trading near an all-time high,” writes Arnott about today.

On the plus side, gold is a millennia-old store of value that can play a role in an investment portfolio. According to Morningstar’s Diversification Landscape Report, gold’s historical correlations to stocks and bonds are low. Like other commodities, it has performed well during inflationary periods, while equities and fixed income have languished. You need not believe that currency debasement is occurring to see gold as a strategic portfolio hedge.

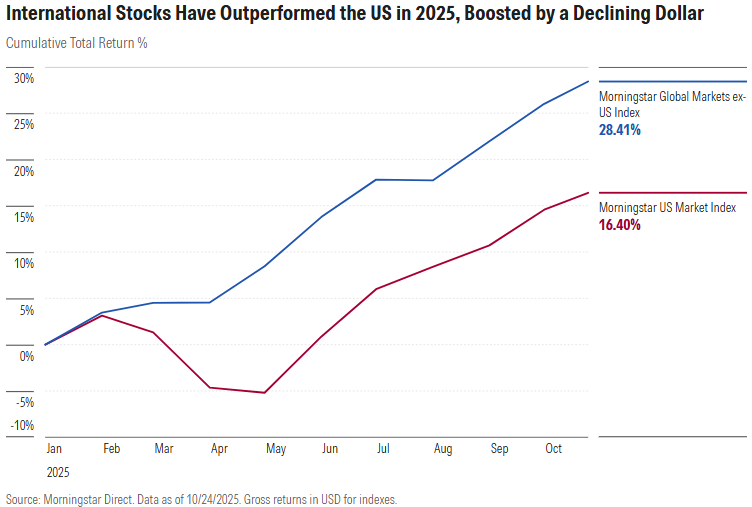

Outperformer #2: International Stocks

Although AI enthusiasm has helped US stocks rebound nicely after their sharp selloff earlier this year, they are still lagging their international counterparts—at least from the perspective of US dollar investors. The Morningstar Global Markets ex-US Index of developed- and emerging-markets equities is well ahead of the Morningstar US Market Index in US dollar terms so far in 2025.

When I look at the returns of the Morningstar Europe Index in euro terms or the Morningstar Japan Index in yen terms, performance is closer to that of US stocks. But those currencies’ appreciation against the dollar in 2025 has amplified gains for unhedged US investors.

Emerging-markets equities have performed even better in 2025, posting returns not seen in 15 years. The Morningstar Korea Index is up more than 75% in dollar terms, and China, Mexico, and Brazil are also booming. Gains have been magnified for US investors because of those currencies strengthening against the dollar.

Will the outperformance of international stocks continue? That’s anyone’s guess. Expert forecasts compiled by my colleague Christine Benz at the start of 2025 uniformly expected international stocks to beat US stocks over the next decade-plus. Based on those projections, upside remains even after the 2025 runup. As I wrote about in August, the US stock market looks top-heavy, high-priced, and low-yield relative to international stocks.

While the diversification benefits of global equities investing have fallen, correlations are changeable. Plus, there are some great companies domiciled across the globe. My colleague Jeff Ptak recently noted that US investor portfolios, in aggregate, are extremely light on international stocks. He characterized their outsize allocations to US equities as “too much of a good thing.” Looking back at history, there have been several periods in which US investors benefited from international exposure.

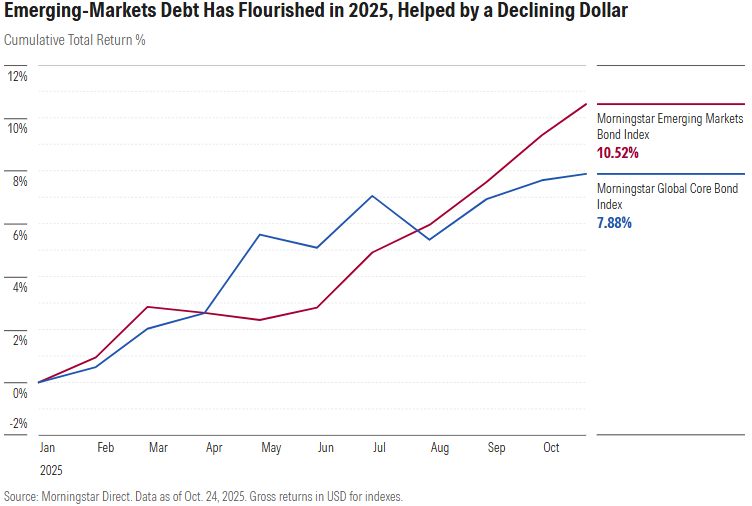

Outperformer #3: Emerging-Markets Debt

Emerging-markets debt has also flourished this year. Even in a strong year for fixed income, it stands out. The Morningstar Emerging Markets Bond Index, which includes US-dollar-denominated debt, has risen more than 10% so far in 2025.

When the dollar falls, that lowers the debt burden for emerging economies borrowing in US currency. Local-currency emerging-markets bonds also gain value for US investors when the currencies they’re denominated in appreciate.

Other factors are boosting the asset class. According to my colleague Gabe Alpert, “rising creditworthiness of emerging-market countries and increasing demand for diversification outside the US” have contributed to gains this year. In some cases, higher commodities prices have also helped. Coming into the year, Morningstar’s 2025 Outlook highlighted compelling valuations and “attractive real yields in the emerging-markets space.”

Even after the strong returns this year, Morningstar Investment Management still finds emerging-markets debt attractive, especially the local-currency variety. They cite high interest rates in many markets, a weaker dollar, and a “supportive macroeconomic backdrop.” While the asset class has tended to post high correlations to equities, making it a poor diversifier, its appeal lies in income and capital appreciation potential. For fixed-income investors, it can add spice to a portfolio.

What’s the Outlook for the US Dollar’s Value?

“Currency forecasters exist to make the weatherman look good.” I was told that once by a fund manager I won’t name, lest he incur the wrath of foreign-exchange traders and meteorologists. Currency values are determined by a complex interplay of variables. Technical factors matter. As the term “foreign exchange” implies, it’s all relative when it comes to currency.

With those caveats out of the way, I’ll recommend an insightful analysis by Muhammad Hamza Saleem of Morningstar Investment Management. Saleem examines five factors, spanning fundamentals and sentiment, that affect the US dollar’s value. He concludes: “In the years ahead, we expect the dollar to gradually depreciate as fiscal strains mount, growth momentum slows, and diversification accelerates. ”According to the team’s models, the dollar looks overvalued today, even after its 2025 decline.

Historically, the dollar has gone through cycles. Arnott describes down periods in the 1970s, late 1980s, and early 2000s. The dollar mostly rose in the 2010s and got a boost in 2022 after the Russian invasion of Ukraine and Federal Reserve interest rate hikes. The weakening we’ve seen in 2025 could be a changing of the tides.

Some see more profound shifts underway. Harvard professor Kenneth Rogoff is among the voices warning of threats to the dollar’s status as the global “reserve currency.” He argues that the dollar’s central role in international finance should not be taken for granted.

From where I sit, you don’t need an outlook to appreciate the logic behind currency diversification. Hedging your bets by investing in asset classes that can thrive when the dollar falls is a sensible strategy. Just look to 2025 as proof.

©2025 Morningstar. All Rights Reserved. The information, data, analyses and opinions contained herein (1) include the proprietary information of Morningstar, (2) may not be copied or redistributed, (3) do not constitute investment advice offered by Morningstar, (4) are provided solely for informational purposes and therefore are not an offer to buy or sell a security, and (5) are not warranted to be correct, complete or accurate. Morningstar has not given its consent to be deemed an "expert" under the federal Securities Act of 1933. Except as otherwise required by law, Morningstar is not responsible for any trading decisions, damages or other losses resulting from, or related to, this information, data, analyses or opinions or their use. References to specific securities or other investment options should not be considered an offer (as defined by the Securities and Exchange Act) to purchase or sell that specific investment. Past performance does not guarantee future results. Before making any investment decision, consider if the investment is suitable for you by referencing your own financial position, investment objectives, and risk profile. Always consult with your financial advisor before investing.

Indexes are unmanaged and not available for direct investment.

Morningstar indexes are created and maintained by Morningstar, Inc. Morningstar® is a registered trademark of Morningstar, Inc.