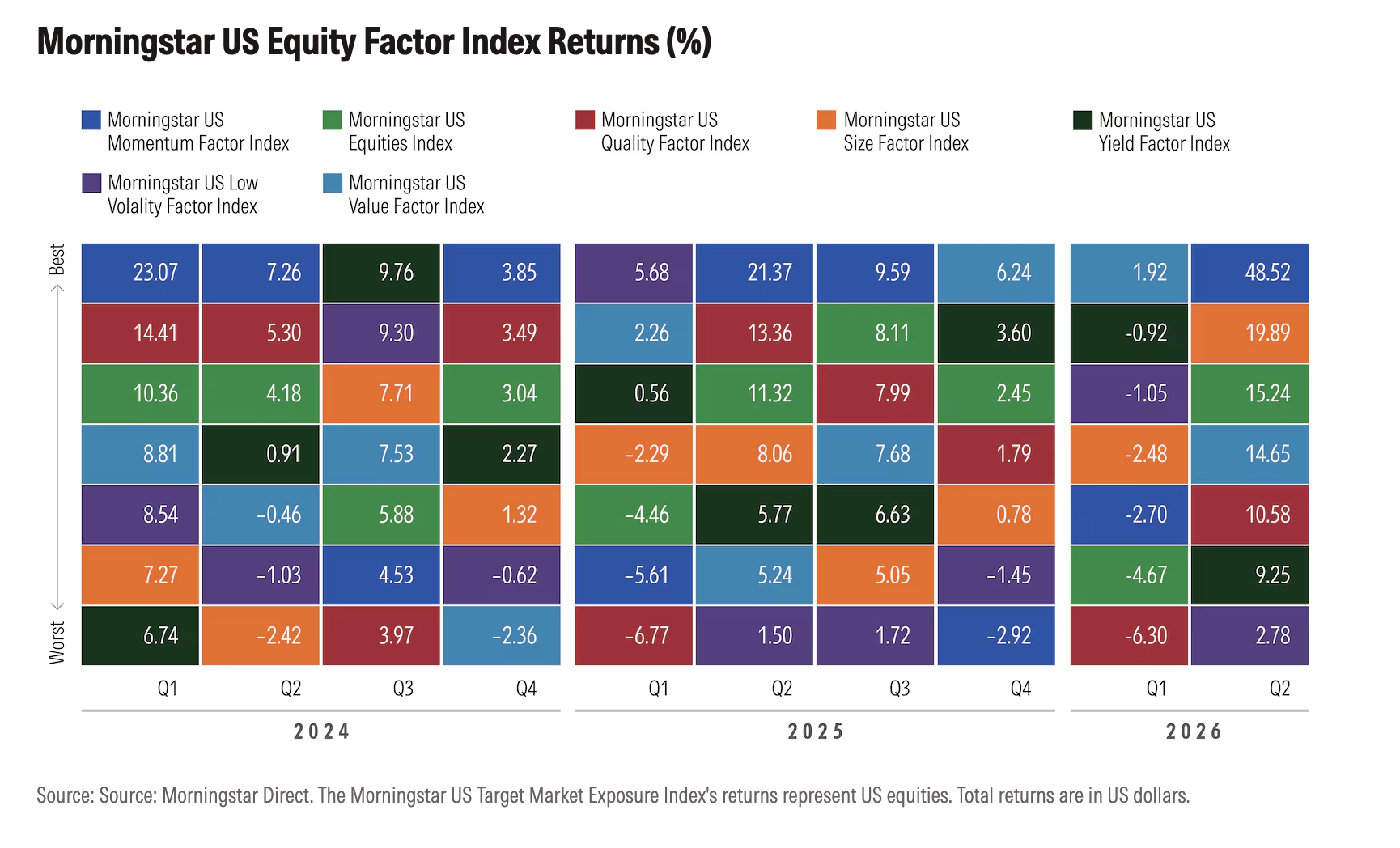

Momentum can be a powerful force in investing. That’s the first thing that pops to mind when looking at the quilt chart below for the Morningstar Factor Indexes, which shows momentum winning in six of the last 10 quarters, including the second quarter of 2026. From April through June, the broad US stock market rebounded from a rough start to the year and gained more than 15%. Investors betting on smaller-sized US companies fared even better, but not as well as those riding the momentum wave.

What’s also interesting is that the quality factor has lagged. That wasn’t just true in the second quarter of 2026. The shares of super-profitable companies with strong balance sheets haven’t beaten the market since the second quarter of 2025. The market’s momentum used to be in quality stocks. But performance dynamics have shifted, with important implications for investors.

The Momentum Factor Is No Longer Surfing the Quality Wave

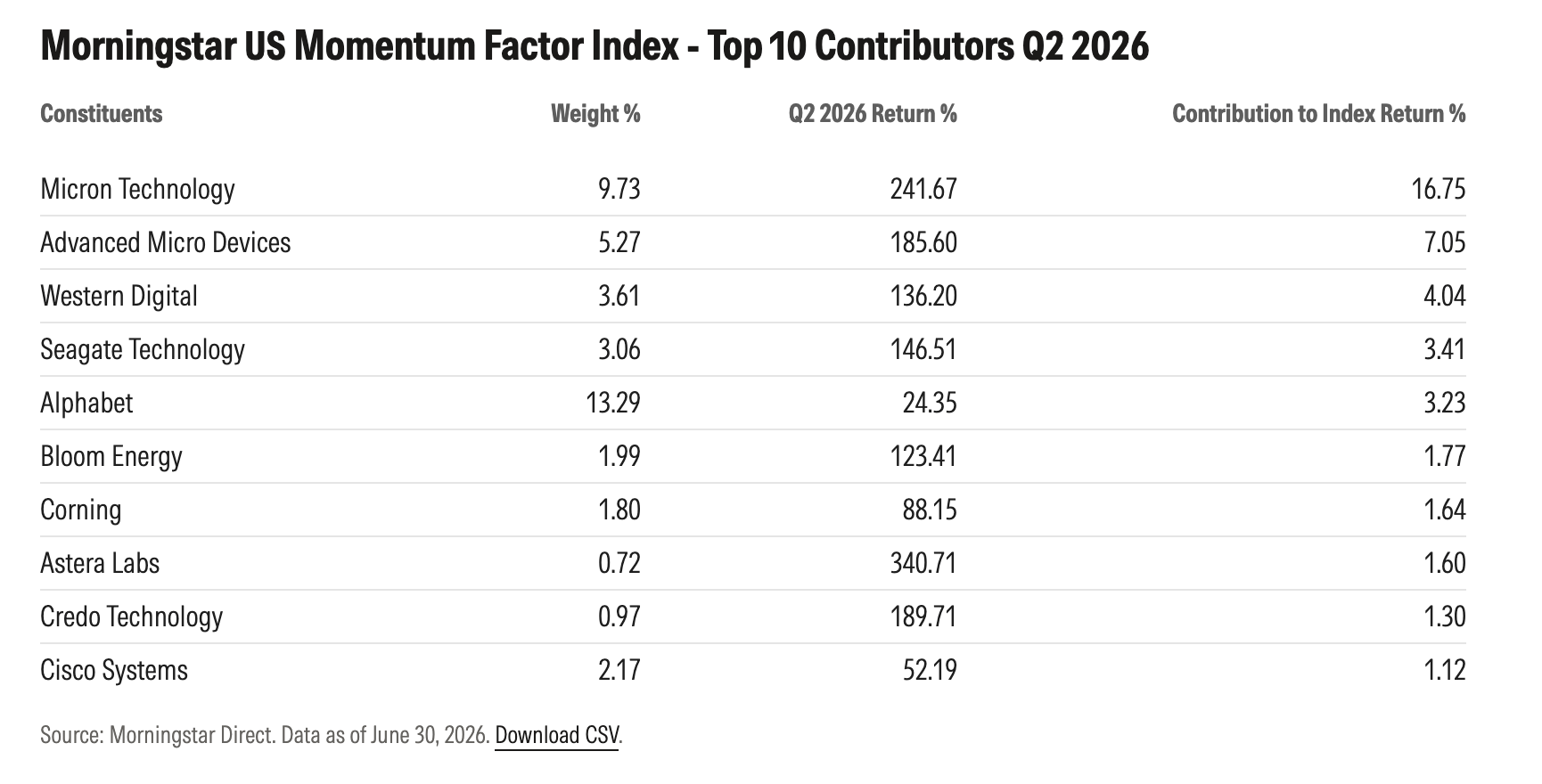

Second-quarter momentum belonged to artificial intelligence stocks. Improbably, several companies joined the “triple-digit club,” meaning their stock prices appreciated by 100%, 200%, or even 300% in just a few months. The 10 biggest contributors to the Morningstar US Momentum Factor Index include semiconductor businesses like Micron MU, AMD AMD, and Lam Research LRCX, memory providers like Western Digital WDC and Seagate Technology STX, and data center supplier Bloom Energy BE. All benefited from a flood of corporate spending on artificial intelligence.

According to a Factor Monitor for the second quarter published by Morningstar Indexes, the momentum in AI stocks was global. Korean chipmaker SK Hynix 000660 also joined the triple-digit club in the second quarter. Advantest 6857 of Japan was another mega-gainer.

Academics who research the momentum factor tell us that investors make a habit of chasing performance. So, some of the second quarter’s triple-digit returns might come from capital piling into hot stocks. But another explanation for investment momentum is that the market can underreact to news. From this perspective, AI stocks’ performance was about share prices catching up to fundamentals. See: Micron’s bumper earnings.

The AI boom also helps explain the strong second-quarter returns for the Morningstar US Size Factor Index, which skews toward smaller companies. Many of its recent winners are suppliers of “picks and shovels” to the AI gold rush. Stocks across the market capitalization spectrum are benefiting.

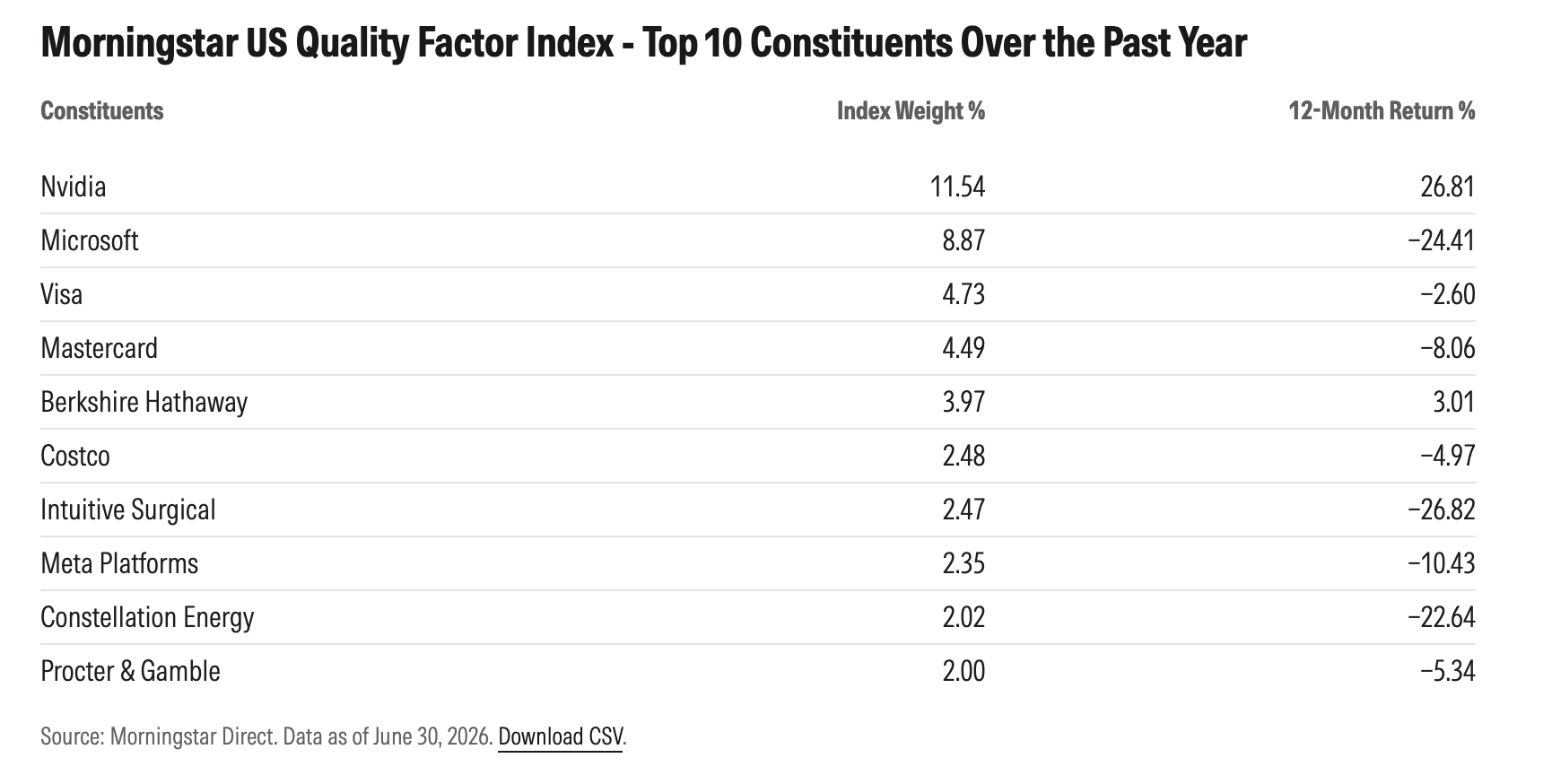

Where momentum has been less evident is with quality stocks—highly profitable companies with strong balance sheets. The factor quilt shows that the Morningstar US Quality Factor Index has lagged—and not just in the second quarter. The losing streak for quality stocks goes back to mid-2025.

That marks a change. Back in October 2025, I wrote that the momentum factor was “surfing a quality wave.” Quality stocks outperformed the market in 2023 and 2024 at the peak of the “Magnificent Seven” era. Over those two years, Nvidia’s NVDA share price appreciated by more than eight times and Meta Platform’s META by a factor of nearly four. When the market bounced back in the second quarter of 2025 from the tariff turmoil of the early part of the year, quality stocks led the charge.

So, what has ailed the quality factor more recently? From a sector perspective, healthcare has been the biggest detractor from the Morningstar US Quality Factor Index’s returns over the trailing 12 months through the second quarter of 2026. There’s also the fading of some members of the Magnificent Seven. Microsoft MSFT and Meta, which both score highly on measures of profitability, have posted poor returns in recent quarters.

Stocks in Motion Tend to Stay in Motion (Until They Don’t)

The knock on momentum is that it works until it doesn’t. Market direction can change on a dime, and when it does, momentum stocks can get whipsawed. According to Philip Straehl, chief investment officer for Morningstar Wealth:

“Our research suggests that periods of strong momentum acceleration increased the likelihood of a reversal. While every market cycle is different, periods of exceptionally strong momentum have often coincided with elevated investor optimism and speculative behavior. Although this may not signal an imminent reversal, it serves as a reminder that parts of the market may be pricing in highly optimistic outcomes.”

Unsurprisingly, the momentum index has been the most volatile of Morningstar’s factor benchmarks, as measured by standard deviation of returns. At market inflection points—most recently, early June 2026—the momentum factor dropped sharply.

March of this year was also difficult for momentum stocks, part of a tricky first quarter. Even before the Iran war and rising energy prices roiled markets, there were fears of artificial intelligence’s disruptive potential, especially related to software businesses. The value, yield, and low volatility factors all outperformed the broad market in the first three months of the year.

Over the past few years, we’ve seen rotations like this before. In both the third quarter of 2024 and the first quarter of 2025, many previously out-of-favor factors outperformed. In the fourth quarter of 2025, the value, yield, and low volatility factors beat the market and extended their runs into the first quarter of 2026. During all of these factor rotations, the broad stock market has produced subdued or negative returns. But in each case, the market has come roaring back, catalyzed by AI stocks.

One clear takeaway from the factor quilt chart is that market leadership is constantly in flux. Quality stocks performed well for years, then lost steam. Only time will tell if market momentum will shift yet again. Perhaps the size factor’s recent resurgence will endure this time.

©2026 Morningstar. All Rights Reserved. The information, data, analyses and opinions contained herein (1) include the proprietary information of Morningstar, (2) may not be copied or redistributed, (3) do not constitute investment advice offered by Morningstar, (4) are provided solely for informational purposes and therefore are not an offer to buy or sell a security, and (5) are not warranted to be correct, complete or accurate. Morningstar has not given its consent to be deemed an "expert" under the federal Securities Act of 1933. Except as otherwise required by law, Morningstar is not responsible for any trading decisions, damages or other losses resulting from, or related to, this information, data, analyses or opinions or their use. References to specific securities or other investment options should not be considered an offer (as defined by the Securities and Exchange Act) to purchase or sell that specific investment. Past performance does not guarantee future results. Before making any investment decision, consider if the investment is suitable for you by referencing your own financial position, investment objectives, and risk profile. Always consult with your financial advisor before investing.

Indexes are unmanaged and not available for direct investment.

Morningstar indexes are created and maintained by Morningstar, Inc. Morningstar® is a registered trademark of Morningstar, Inc.